With effect from 12 Jan 2013, a comprehensive package of measures has been introduced to cool the residential property market. The Government has also introduced a Seller’s Stamp Duty on industrial properties for the first time, to discourage speculative activity in the industrial market.

SUMMARY

A) Cooling Measures for the Residential Property Market

The following measures will take effect on 12 January 2013:

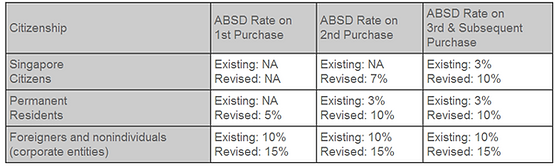

1. Additional Buyer's Stamp Duty (ABSD) rates will be:

- Raised between five and seven percentage points across the board.

- Imposed on Permanent Residents (PRs) purchasing their first residential property and on Singaporeans purchasing their second residential property.

7th ROUND OF COOLING MEASURES (2013)

Read the full article below, or download the PDF here.

Additional Measures to Ensure a Stable and Sustainable Property Market

11 Jan 2013 07:00 PM

Issued by the Ministry of Finance, Ministry of National Development, Monetary Authority of Singapore and Ministry of Trade & Industry

1 The Government announced today a comprehensive package of measures to cool the residential property market. It also introduced a Seller’s Stamp Duty on industrial properties for the first time, to discourage speculative activity in the industrial market.

Cooling Measures for the Residential Property Market

2 The Government has implemented several rounds of measures to cool demand and expand supply, so as to moderate the increase in housing prices. While these measures have dampened speculative buying, the demand for residential property remains firm and prices have continued to rise.

3 The continued buoyancy of the property market reflects the very low interest rate environment and continued income growth in Singapore. These factors supported a record level of housing transactions last year, particularly from investment demand. Housing prices have also shown signs of reaccelerating in recent months, in both the private residential and HDB resale flat markets. Price increases, if not checked, will run further ahead of economic fundamentals and raise the risk of a major, destabilising correction later on.

4 The Government has therefore decided to implement a further set of measures to cool the private and public housing markets. These measures are calibrated to be tighter on property ownership for investment, as well as on foreign buyers. To discourage over-borrowing, financing conditions for housing have also been tightened. In addition, structural measures have been implemented to strengthen the policy intent of public housing and Executive Condominiums (ECs).

5 Deputy Prime Minister and Minister for Finance Mr Tharman Shanmugaratnam said: “The reality we face is that interest rates are extraordinarily low, globally and in Singapore, and continue to add fuel to our property market. We have to take this further round of measures now, to check recent market trends and avoid a more serious correction in prices further down the road.”

6 Minister for National Development Mr Khaw Boon Wan said: “A large supply of public and private housing – up to 200,000 units in total – will be completed in the coming years. Coupled with the new measures, we will be better placed to ensure that housing remains affordable to Singaporeans.”

Measures Applicable to all Residential Property

7 The following measures will take effect on 12 January

a) Additional Buyer’s Stamp Duty (ABSD) rates will be

i) Raised between five and seven percentage points across the board.

ii) Imposed on Permanent Residents (PRs) purchasing their first residential property and on Singaporeans purchasing their second residential property.

b) Loan-to-Value limits on housing loans granted by financial institutions will be tightened for individuals who already have at least one outstanding loan, as well as to non-individuals such as companies.

c) Besides tighter Loan-to-Value limits, the minimum cash down payment for individuals applying for a second or subsequent housing loan will also be raised from 10% to 25%.

8 The measures listed above will not impact most Singaporeans buying their first home. Some concessions will also be extended to selected groups of buyers, such as married couples with at least one Singaporean spouse who are purchasing their second property and will sell their first residential property.

9 The new ABSD and loan rules are significant, but they are temporary. They are being imposed to cool the market now, and will be reviewed in the future depending on market conditions.

10 The details of the ABSD measure are set out in Annex I and the housing loan measures, in Annex II.

Measures Specific to Public Housing

11 The Government is also introducing measures to further moderate the demand for HDB flats, instil greater financial prudence among buyers, and require owner occupation by PR buyers. The following measures will take effect on 12 January 2013:

a) Tighter eligibility for loans to buy HDB flats:

i) MAS will cap the Mortgage Servicing Ratio (MSR) for housing loans granted by financial institutions at 30% of a borrower’s gross monthly income.

ii) For loans granted by HDB, the cap on the MSR will be lowered from 40% to 35%.

b) PRs who own a HDB flat will be disallowed from subletting their whole flat.

c) PRs who own a HDB flat must sell their flat within six months of purchasing a private residential property in Singapore.

Details of these measures are in Annex III.

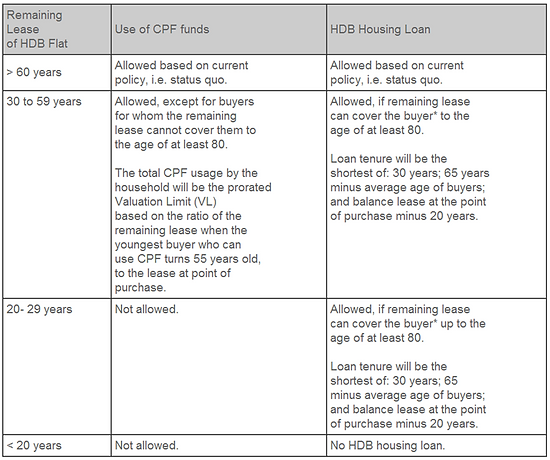

12 An additional measure will take effect on 1 July 2013 to tighten the terms for granting HDB loans and the use of CPF funds for the purchase of HDB flats with remaining leases of less than 60 years (details of this measure are in Annex IV).

Measures for Executive Condominium Developments

13 The Government will introduce measures specific to new EC developments to ensure that ECs continue to serve as an affordable housing option for middle-income Singaporean families.

14 The following measures will take effect on 12 January 2013:

a) The maximum strata floor area of new EC units will be capped at 160 square metres.

b) Sales of new dual-key EC units will be restricted to multi-generational families only.

c) Developers of future EC sale sites from the Government Land Sales programme will only be allowed to launch units for sale 15 months from the date of award of the sites or after the physical completion of foundation works, whichever is earlier.

d) Private enclosed spaces and private roof terraces will be treated as gross floor area (GFA). The GFA of such spaces in non-landed residential developments, including ECs, will be counted as part of the ‘bonus’ GFA of a residential development and subject to payment of charges. This is in line with the treatment of balconies under URA’s current guidelines. Details of this measure are at www.ura.gov.sg/circulars/text/dc13-01.htm.

Cooling Measure for the Industrial Property Market: Seller’s Stamp Duty

15 Prices of industrial properties have doubled over the last three years, outpacing the increase in rentals. In addition, there has been increasing speculation in industrial properties: in 2011 and the first eleven months of 2012, about 15% and 18% respectively of all transactions of multiple-user factory space were resale transactions carried out within three years of purchase. This is significantly higher than the average of about 10% from 2006 to 2010.

16 The Government is introducing Seller’s Stamp Duty (SSD) on industrial property to discourage short-term speculative activity which could distort the underlying prices of industrial properties and raise costs for businesses.

17 With effect from 12 January 2013, the following SSD rates will be imposed on industrial properties and land bought and sold within three years of the date of purchase:

a) SSD at 15% if the property is sold in the first year of purchase, i.e. the property is held for one year or less from the date of purchase.

b) SSD at 10% if the property is sold in the second year of purchase, i.e. the property is held for more than one year and up to two years from the date of purchase.

c) SSD at 5% if the property is sold in the third year of purchase, i.e. the property is held for more than two years and up to three years from the date of purchase.

18 The Inland Revenue Authority of Singapore (IRAS) will be releasing an E-tax guide on the circumstances under which SSD is applicable and the procedures for paying SSD. The E-tax guide will be available at www.iras.gov.sg.

Source: Ministry of National Development (MND)

2. Loan-to-Value limits on housing loans granted by financial institutions will be tightened for individuals who already have at least one outstanding loan, as well as to non-individuals such as companies.

3. Besides tighter Loan-to-Value limits, the minimum cash down payment for individuals applying for a second or subsequent housing loan will also be raised from 10% to 25%.

B) Cooling Measures Specific to Public Housing

1. Tighter eligibility for loans to buy HDB flats:

- MAS will cap the Mortgage Servicing Ratio (MSR) for housing loans granted by financial institutions at 30% of a borrower's gross monthly income.

- For loans granted by HDB, the cap on the MSR will be lowered from 40% to 35%.

2. PRs who own a HDB flat will be disallowed from subletting their whole flat.

3. PRs who own a HDB flat must sell their flat within six months of purchasing a private residential property in Singapore.

4. An additional measure will take effect on 1 July 2013 to tighten the terms for granting HDB loans and the use of CPF funds for the purchase of HDB flats with remaining leases of less than 60 years.

C) Cooling Measures for Executive Condominium Developments

The following SSD rates will be imposed on industrial properties and land bought and sold within three years of the date of purchase:

a) The maximum strata floor area of new EC units will be capped at 160 square metres.

b) Sales of new dual-key EC units will be restricted to multi-generational families only.

c) Developers of future EC sale sites from the Government Land Sales programme will only be allowed to launch units for sale 15 months from the date of award of the sites or after the physical completion of foundation works, whichever is earlier.

d) Private enclosed spaces and private roof terraces will be treated as gross floor area (GFA). The GFA of such spaces in non-landed residential developments, including ECs, will be counted as part of the 'bonus' GFA of a residential development and subject to payment of charges. This is in line with the treatment of balconies under URA's current guidelines.

D) Cooling Measure for the Industrial Property Market: Seller's Stamp Duty

The following SSD rates will be imposed on industrial properties and land bought and sold within three years of the date of purchase:

a) SSD at 15% if the property is sold in the first year of purchase, i.e. the property is held for one year or less from the date of purchase

b) SSD at 10% if the property is sold in the second year of purchase, i.e. the property is held for more than one year and up to two years from the date of purchase.

c) SSD at 5% if the property is sold in the third year of purchase, i.e. the property is held for more than two years and up to three years from the date of purchase.

Read the full article below, or download the PDF here.

MAS Introduces Debt Servicing Framework for Property Loans

28 Jun 2013 07:00 PM

Issued by the Monetary Authority of Singapore

The Monetary Authority of Singapore (MAS) will introduce a Total Debt Servicing Ratio (TDSR) framework for all property loans granted by financial institutions (FIs) to individuals1. This will require FIs to take into consideration borrowers’ other outstanding debt obligations when granting property loans. They will help strengthen credit underwriting practices by FIs and encourage financial prudence among borrowers.

2 MAS will also refine rules related to the application of the existing Loan-to-Value (LTV) limits on housing loans. These refinements seek to ensure the effectiveness of the LTV limits that were put in place to cool investment demand in the housing market. In particular, they aim to prevent circumvention of the tighter LTV limits on second and subsequent housing loans.

Introduction of TDSR framework

3 MAS conducted a thematic inspection of banks’ residential property loan portfolios in 2012. While banks generally had in

place sound policies to assess the credit worthiness of borrowers, the inspection and subsequent surveys revealed uneven practices with respect to the application of debt servicing ratios and highlighted areas for improvement in credit underwriting practices.

4 The TDSR framework will provide FIs a robust basis for assessing the debt servicing ability of borrowers applying for property loans, taking into consideration their other outstanding debt obligations. FIs will be required to compute the TDSR, or the percentage of total monthly debt obligations to gross monthly income, on a consistent basis.2

5 The coverage of the TDSR framework will be more comprehensive than FIs’ current practice. The TDSR will apply to loans for the purchase of all types of property, loans secured on property,3 and the re-financing of all such loans.4

6 The methodology for computing the TDSR will be standardised. FIs will be required to:

-

take into account the monthly repayment for the property loan that the borrower is applying for plus the monthly repayments on all other outstanding property and non-property debt obligations of the borrower;

-

apply a specified medium-term interest rate or the prevailing market interest rate, whichever is higher, to the property loan that the borrower is applying for when calculating the TDSR;5

-

apply a haircut of at least 30% to all variable income (e.g. bonuses) and rental income; and apply haircuts

6 to and amortise the value of any eligible financial assets taken into consideration in assessing the borrower’s debt servicing ability, in order to convert them into ‘income streams’ in computing the TDSR.

7 FIs will be required to verify and obtain relevant documentation on a borrower’s debt obligations and income used in the computation of the TDSR.

8 MAS expects any property loan extended by the FI to not exceed a TDSR threshold of 60% and will regard any property loan in excess of a 60% TDSR to be imprudent.7 The threshold is set at 60% for a start to allow both the FIs and borrowers to familiarise themselves with the TDSR framework and its computation methodology. MAS will monitor and review the 60% threshold over time, with a view to further encouraging financial prudence.

Refinement of rules related to application of LTV limits

9 MAS will refine certain rules related to the application of the existing LTV limits on housing loans granted by FIs. In particular, MAS will require:

-

borrowers named on a property loan to be the mortgagors of the residential property for which the loan is taken;

-

“guarantors” who are standing guarantee for borrowers otherwise assessed by the FI at the point of application for the housing loan not to meet the TDSR threshold for a property loan to be brought in as co-borrowers; and

-

in the case of joint borrowers, that FIs use the income-weighted average age of borrowers8 when applying the rules on loan tenure.9

Measures for the long term

10 The new rules will take effect from 29 June 2013.

11 The TDSR framework and refinements to the rules relating to the application of LTV limits are structural in nature, and will be in place for the long term. They aim to encourage prudent borrowing by households and strengthen credit underwriting standards by FIs.

12 They do not involve changes to the LTV limits on housing loans themselves, which were last tightened in January 2013 as part of the government’s package of measures to promote stable and sustainable conditions in the housing market.10

The current LTV limits are not permanent, and will be reviewed depending on the state of the property market.

13 Please refer to the FAQs on MAS’ website for further details.

***

1 This includes sole proprietorships and vehicles set up by an individual solely to purchase property.

2 In the case of a joint application for a property loan, the TDSR shall be computed based on the aggregate total monthly debt obligations and aggregate gross monthly incomes of the joint borrowers.

3 Where a loan is secured by a pool of collateral including property, the TDSR rules will apply if the market value of the property is 50% or more of the value of the total pool of collateral.

4 Existing borrowers who are seeking to refinance their housing loans will be exempted, provided they meet the specific conditions set out in MAS’ Guidelines on the Application of TDSR for Property Loans under MAS Notices 645, 1115, 831 and 128.

5 3.5% for housing loans and 4.5% for non-residential property loans.

6 Eligible liquid assets which are pledged for at least 4 years with the FI from which the borrower is taking the property loan will not be subject to any haircut.

7 Property loans in excess of the TDSR threshold of 60% should be granted only on an exceptional basis. The board of directors of the FI (or senior management in the case of an FI incorporated outside of Singapore) will have to approve policies and procedures relating to such exceptions. In addition, cases exceeding the threshold will need to be approved by the FI’s credit committee.

8 The income-weighted average age will be based on the borrowers’ gross monthly income.

9 Lower LTV limits apply to a loan granted for the purchase of a residential property, where the loan period extends beyond the retirement age of 65 years or the tenure exceeds 30 years.

10 In January 2013, MAS lowered the LTV limits for housing loans to individuals with one outstanding housing loan from 60% to 50%, and to individuals with two or more outstanding housing loans from 60% to 40%. Loans with longer tenure faced even tighter LTV limits. The LTV limit for housing loans to non-individuals was also reduced to 20%.

DEBT SERVICING FRAMEWORK FOR PROPERTY LOANS (2013)

With effect from 29 June 2013, the Monetary Authority of Singapore (MAS) will introduce a Total Debt Servicing Ratio (TDSR) framework for all property loans granted by financial institutions (FIs) to individuals and also refine rules related to the application of the existing Loan-to-Value (LTV) limits on housing loans.